Introduction: Tax season in India can often be a daunting period, but it doesn’t have to be that way. With proper planning and knowledge, individuals can navigate the complex tax landscape and make the most of available deductions and exemptions. In this comprehensive guide, we will explore the top tax-saving strategies for individuals in India, helping you minimize your tax liability while maximizing your financial well-being.

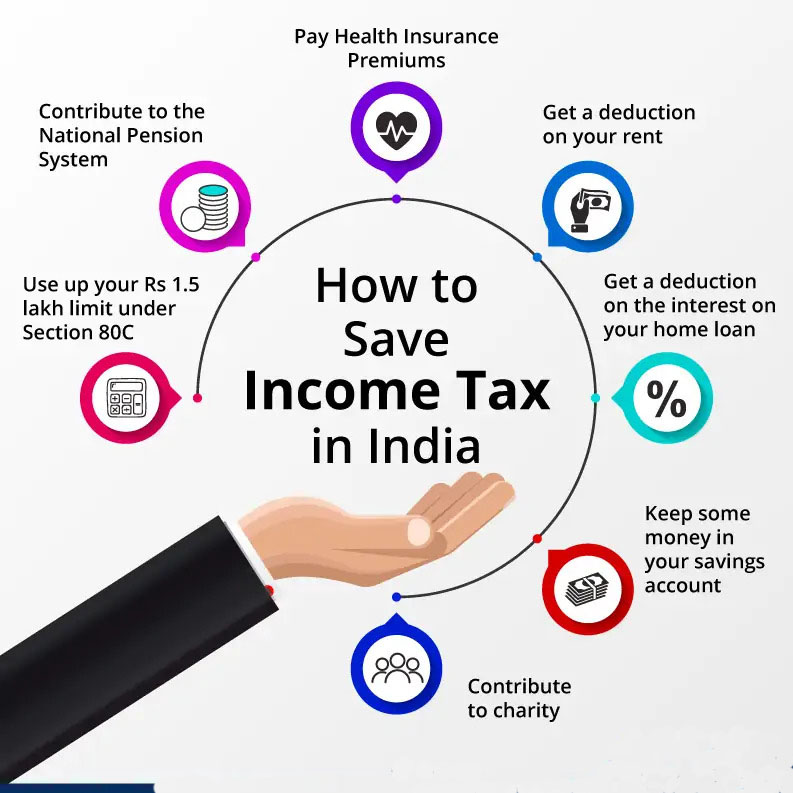

Section 80C: A Treasure Trove of Tax Savings Section 80C of the Income Tax Act serves as a treasure trove of tax-saving opportunities. This section allows individuals to claim deductions up to ₹1.5 lakh on various investments and expenditures. Among the most popular options are:

- Employee Provident Fund (EPF): For salaried individuals, contributing to EPF not only builds a retirement corpus but also offers tax benefits. Your EPF contributions are eligible for deductions under Section 80C.

- Public Provident Fund (PPF): The PPF is a long-term savings instrument that not only provides attractive interest rates but also offers tax exemptions on both contributions and interest earned.

- National Savings Certificate (NSC): Invest in NSC, a fixed-income savings scheme offered by India Post. The principal amount invested in NSC qualifies for deductions under Section 80C.

- Tax-Saving Fixed Deposits: Many banks offer tax-saving fixed deposits with a lock-in period of five years. The interest earned is taxable, but the principal amount invested is deductible under Section 80C.

- Equity-Linked Savings Scheme (ELSS): ELSS funds offer the dual advantage of potential capital appreciation and tax savings. Invest in these mutual funds and enjoy deductions under Section 80C.

Health is Wealth: Leveraging Health Insurance Securing health insurance not only ensures your well-being but also brings tax benefits. Under Section 80D, individuals can claim deductions on the premiums paid towards health insurance policies:

- Self, Family, and Parents: Premiums paid for health insurance covering yourself, your family, and your parents are eligible for deductions. The limit varies based on the age of the insured individuals.

- Preventive Health Checkups: In addition to health insurance premiums, expenses related to preventive health checkups are also eligible for deductions under Section 80D.

Home Loan Interest: A Deduction Worth Noting For individuals with home loans, the interest paid on the loan can lead to substantial tax benefits. Under Section 24(b), you can claim deductions on the interest paid:

- Self-Occupied Property: If you reside in the property for which the home loan is taken, you can claim up to ₹2 lakh in deductions on the interest paid.

- Let-Out Property: If you let out the property, there is no upper limit on the deduction for interest paid on the home loan.

National Pension System (NPS): Planning for Retirement and Tax Savings The National Pension System (NPS) is a versatile tool that not only helps in retirement planning but also offers tax advantages. Under Section 80CCD(1B), both salaried individuals and self-employed professionals can claim deductions on NPS contributions:

- Salaried Employees: Salaried individuals contributing to NPS can claim deductions of up to 10% of their salary (basic + DA) under Section 80CCD(1) within the overall limit of ₹1.5 lakh under Section 80C.

- Self-Employed Individuals: Self-employed individuals can also claim deductions on their NPS contributions under Section 80CCD(1B), subject to the same overall limit of ₹1.5 lakh under Section 80C.

House Rent Allowance (HRA): Maximizing Exemptions For individuals receiving House Rent Allowance (HRA) as a part of their salary, there are ways to maximize exemptions:

- Actual Rent Paid: Claim exemptions on the actual rent paid, minus 10% of your salary. This is applicable if the rent paid exceeds 10% of your salary.

- HRA Received: If the HRA received is less than the actual rent paid, the balance amount can be claimed as an exemption under Section 10(13A).

Strategic Donations: Giving Back and Saving Taxes Contributing to charitable causes not only makes a positive impact on society but also offers tax benefits. Donations made to registered charitable organizations can lead to deductions under Section 80G:

- Eligible Donations: Understand the types of donations that qualify for deductions and the applicable limits. Some donations are eligible for 100% deduction, while others may be subject to specific limits.

- Collect Receipts: Ensure you collect proper receipts and documentation for the donations made, as these will be required for claiming deductions.

The New Tax Regime: Evaluating Your Options The Budget 2020 introduced a new tax regime that offers lower tax rates in exchange for foregoing certain exemptions and deductions. Individuals now have the option to choose between the old regime with deductions or the new regime with lower tax rates:

- Old Tax Regime: Under the old regime, individuals can continue to claim deductions under various sections, including 80C, 80D, and 24(b).

- New Tax Regime: The new regime offers reduced tax rates but eliminates many exemptions and deductions. Individuals need to carefully assess which regime aligns better with their financial situation.

Tax-Deferred Investments: Planning for the Future Certain tax-saving investments come with longer lock-in periods but offer significant benefits:

- Sukanya Samriddhi Yojana (SSY): Invest in SSY for your girl child’s education and marriage. Contributions to SSY are eligible for deductions under Section 80C, and the interest earned is tax-free.

- Senior Citizens Savings Scheme (SCSS): This scheme is tailored for retirees, offering regular interest payments and deductions on investments under Section 80C.

Conclusion: Navigating the world of tax-saving strategies requires careful consideration and planning. By implementing these top tax-saving strategies, individuals in India can optimize their financial resources, reduce their tax liabilities, and achieve their long-term financial goals. However, it’s crucial to remember that tax laws and regulations may change over time, so seeking advice from a qualified tax consultant is essential to ensure that your strategies remain aligned with the latest regulations.

Empower yourself with knowledge, make informed financial decisions, and embark on a journey toward a more secure and prosperous financial future.

{kind=link}